Jordan Schwartz on Building Long-Term Client Trust and Thriving as a Fractional GC

Jordan Schwartz is a seasoned in-house attorney with Big Law roots and experience as a General Counsel. Since transitioning into freelance work, he has partnered with a range of dynamic, high-growth companies, helping to scale their businesses while managing diverse legal functions—including tech transactions, product counseling, intellectual property, and general corporate matters.

Tell us a bit about your professional background.

I worked at a large NYC law firm after law school, then joined a startup in Silicon Valley as their GC prior to transitioning back to private practice.

What encouraged you to start your own solo practice?

As a GC, I was frustrated by the lack of options available to a small, rapidly growing company, which were limited to working with larger law firms at relatively high rates with work typically done by junior lawyers, or expanding the legal team. Seeing a gap in the market for experienced, hybrid lawyers, who are external to the company but can plug-in and work with other internal stakeholders like in-house counsel, I decided to explore if that model would work, especially in light of the changing technological landscape that enables lawyers to be able to work remotely.

When did you first learn about Lawtrades and what prompted you to join the platform?

Around 2019-2020. It appeared to be a good platform for reaching a diverse group of early- and mid-stage companies, especially in geographic regions outside my immediate area. I also appreciated it taking some of the admin work of running a small firm, such as with client billings.

What's your favorite aspect of Lawtrades?

Access to high quality clients, but at an early enough stage where I can develop and grow the relationships over several years.

What advice would you have for others that are looking to utilize Lawtrades successfully?

If you are just starting out, be willing to be flexible with opportunities in order to establish a baseline of clients and to find the right work balance for the number of hours you are looking to get to work. Hopefully you will be able to find longer term clients that will engage your services over several years like many of mine have, which helps reduce downtime as an individual client's work fluctuates throughout the year, and also allows you to gradually reach any additional income goals by taking on new clients and/or increasing rates.

How do you establish strong, long-term relationships with clients?

First and foremost, basic professional requirements are always key, like performing work diligently and in a timely manner. But also strong communication skills and willingness to tailor your services depending on each client's particular situation and needs. For example, some clients may have fairly loose processes with little guidance, whereas other client's processes will be more rigorous and standardized. Each client also has different levels of risk tolerance and particular contractual terms they are sensitive to, so try to calibrate your approach as quickly as possible to what each specific client's needs are, not just what you may be used to from past work.

Ultimate Guide to Legal Spend Analytics Platforms

Your legal expenses are climbing fast. What once felt like manageable overhead now eats into budgets meant for product development, growth, and innovation. You've tried tightening review cycles, renegotiating with firms, and even freezing specific projects. But nothing seems to hold back the tide.

You're not alone. A recent ACC Law Department report revealed that the median total legal spend jumped from $2.4 million to $3.1 million in just one year. That’s a 29 percent increase without a matching rise in headcount or bandwidth.

Many legal teams are now turning to a more innovative solution.

Legal spend analytics platforms are designed to turn complex billing data into clear, strategic insights. These tools help you take control of your budget, eliminate waste, and plan appropriately.

This guide explains exactly how they work and how to use them to make your legal department more efficient, responsive, and cost-aware.

Core Platform Features

Legal spend analytics platforms offer a focused set of features designed to make financial oversight smarter and more efficient. These features are why legal teams can rely on them for budget control, forecasting, and performance monitoring. Here's what makes them essential.

Expense Tracking Tools

These systems collect, categorize, and centralize billing data from law firms, internal teams, and vendors. Invoices, time entries, and matter-specific charges are captured with minimal manual input, giving legal departments complete visibility into where money is going. Such clarity helps enforce billing guidelines and surface cost drivers, and detect inefficiencies across workflows.

Data Visualization Options

Once data is consolidated, it is transformed into intuitive dashboards that present financial information in ways that legal and business stakeholders can easily understand. These dashboards highlight spending by firm, matter, region, or department. They also track budget adherence and reveal changes over time. Filters and custom views help teams drill down into key metrics, compare performance, and quickly identify areas that need attention.

Machine Learning Applications

Built-in machine learning models take analysis a step further. By studying past spending patterns, they forecast future legal costs, detect unusual billing behaviors, and recommend ways to reduce spending. This predictive capability gives teams an edge in budget planning, rate negotiations, and long-term resourcing decisions.

Custom Approval Workflows

Many platforms allow legal departments to configure approval paths that reflect internal policies. These workflows help ensure every invoice is correctly reviewed before payment, reducing the risk of overbilling or unauthorized charges. This control feature supports compliance and improves accountability at every stage of spend management.

Integration with Financial Systems

Legal spend tools often integrate with ERP and accounting software, enabling seamless data transfer across systems. This reduces manual reconciliation, improves accuracy, and ensures finance and legal teams are working from a shared view of the numbers.

These features transform legal spend from scattered data points into actionable intelligence.

Platform Size and Customization

Legal spend analytics platforms are built to support teams at any growth stage. Whether managing a lean legal function or operating across multiple regions, these platforms scale in functionality and complexity, allowing you to maintain financial control as operations expand.

Solutions by Company Size

Scalability means different teams can start where they are and grow without switching systems. Smaller departments often begin with essential tools to centralize invoices and automate approval workflows. For example, a three-person legal team might use the platform to route all incoming invoices to one approver and apply basic spend caps per vendor.

Midsize legal teams need more advanced functionality. They benefit from department-specific reporting, quarterly trend analysis, and policy enforcement across units. A regional office may need to track litigation spending separately from M&A costs while sharing overall insights with headquarters.

Large enterprises require the most customization and analytics depth. These teams often work across jurisdictions and currencies, with dozens of matter types and hundreds of external vendors. For example, a global pharmaceutical company may use the platform to standardize billing compliance across North America, Europe, and Asia while allowing each region to run its own internal reports.

To get the most value, match platform capabilities to team structure:

- Small teams should prioritize tools for invoice intake, expense tagging, and simple approval logic.

- Midsize departments benefit from tracking accruals, setting up rules for recurring matters, and customizing templates for executive reporting.

- Large legal operations often need role-based permissions, integration with ERP systems, and dashboards that consolidate spending by geography, matter category, and business unit.

Custom Platform Setup

Customization transforms a standard product into a legal operations asset. Teams can align the platform with internal policies, workflows, and reporting goals to ensure the analytics reflect their actual operating environment.

Steps to customize effectively:

- Create reports by legal service area (e.g., IP, litigation, regulatory) or region.

- Define billing thresholds that auto-flag timekeepers exceeding agreed hourly rates.

- Configure roles to route invoices from certain vendors to the appropriate reviewers.

- Sync legal data outputs with finance platforms such as NetSuite or SAP for consolidated budget tracking.

Customization Needs by Size

| Company Size | Common Customization Needs |

|---|---|

| Small Teams | Basic expense tracking, simple approval workflows |

| Mid-size Organizations | Department-specific reports, flexible billing compliance |

| Large Enterprises | Complex workflow automation, multi-department analytics |

By combining scalability with meaningful customization, legal spend analytics platforms help legal departments operate with precision, transparency, and adaptability, regardless of size or structure.

Platform Advantages

Legal spend analytics platforms provide legal departments with the infrastructure to manage costs strategically. Their practical features streamline decision-making, eliminate waste, and improve financial visibility across matters, vendors, and departments.

Spending Control

These platforms make it easier to identify patterns, outliers, and opportunities for cost reduction. With centralized dashboards and alerts for out-of-budget activity, teams can make quicker adjustments and maintain tighter control over expenditures. This clarity allows for faster decisions when reallocating funds or negotiating fee arrangements.

Data-Based Planning

By converting historical data into usable intelligence, legal teams can forecast future spending more confidently. Forecasting tools guide annual budgeting processes and help prioritize investments across internal and external resources. With clearer financial baselines, leaders are better equipped to make long-term resource decisions.

Billing Compliance

Built-in guardrails help ensure all billing activity adheres to outside counsel guidelines. Automated flagging of non-compliant charges reduces the need for manual review and keeps billing cycles efficient and auditable.

Workflow Efficiency

These platforms reduce administrative burdens and accelerate routine tasks by eliminating manual processes. Legal teams can process invoices, generate reports, and respond to finance queries quickly, freeing up bandwidth for strategic work.

Vendor Performance Benchmarking

Some platforms offer scorecard features that evaluate law firm performance based on cost, outcome, and adherence to guidelines. Such data helps legal departments choose partners based on value delivered, not just hours billed.

These platforms create a measurable impact by connecting day-to-day financial processes with strategic decision-making, helping legal departments reduce waste, increase accuracy, and scale confidently.

Steps to Get Started

You're ready to bring legal spend analytics into your workflow, but where should you begin? The key is to move forward with a plan that fits your team's structure, meets your operational needs, and supports your long-term growth. Here’s how to approach it effectively:

1. Define Operational Needs Clearly

Begin with a clear assessment of what your legal department needs today. Evaluate your current pain points: Are you struggling with manual invoice review? Do you lack visibility into firm-level spending? Are budgets consistently inaccurate or difficult to track? Factor in your team size, internal capabilities, and volume of legal matters. Then match these requirements with platform capabilities such as automation features, customizable dashboards, and reporting formats. Ensure the platform fits your legal operations and integrates well with your finance and procurement systems.

2. Plan for Scalable Use

Choose a platform that evolves as your team and business grow. Look for flexibility in user management, matter volume, and integrations. The system should support future expansion, whether onboarding more departments, adding regions, or automating new processes without disrupting existing workflows.

3. Train Your Team Thoroughly

Invest in comprehensive training for both legal and operations users. Ensure your team understands how to use the dashboards, configure reports, and interpret forecasts. Assign internal champions who can provide guidance and liaise with your platform provider when needed. Effective onboarding improves adoption and minimizes downtime.

4. Leverage Support Resources

Don’t implement alone. Work closely with vendor success teams, use onboarding checklists, and consult available documentation. Support teams can help tailor the platform to your requirements and troubleshoot early challenges, ensuring smoother deployment and faster ROI.

5. Set Performance Benchmarks Early

Define what success looks like from day one. Set KPIs like reduced invoice processing time, improved forecast accuracy, or a specific reduction in outside counsel spend. These benchmarks help your team stay focused, measure platform impact, and confidently report results to leadership.

6. Start with a Pilot Rollout

Instead of deploying company-wide immediately, begin with a small-scale pilot. Select a few departments to test workflows, validate assumptions, and capture user feedback. Use knowledge to fine-tune the setup before scaling across the organization.

Conclusion: Repositioning Legal Spend as a Strategic Lever

Legal spend is one of the most under-optimized functions in corporate legal departments. Without structured systems for tracking, forecasting, and analyzing costs, budget planning becomes reactive, value measurement remains vague, and decision-making lacks precision.

Legal spend analytics platforms are designed to resolve this by embedding structure into how legal departments manage cost and performance. Centralized billing data, automated compliance reviews, and predictive insights enable evaluating vendor efficiency, allocating resources based on real need, and accurately anticipating future budget demands.

Legal teams need support structures that adapt as priorities shift to fully operationalize these insights. This includes access to legal professionals who understand how to align with internal systems, consistently apply billing guidelines, and close resource gaps without disrupting workflows.

Lawtrades enables that flexibility. It connects teams to experienced attorneys who can work within analytics platforms to execute more innovative legal spend strategies. Whether optimizing rate structures, managing overflow work, or validating invoice data, this embedded expertise ensures that analytics translate into action.

The result is a shift from fragmented spending oversight to a controlled, strategic process that scales with the business. Legal operations become measurable, defensible, and aligned with long-term goals, with spending actively directed rather than simply recorded.

Related posts

How AI Improves Document Review Protocols

Reviewing legal documents manually is like searching for a single book in an unorganized library; it takes hours of effort, drains energy, and often ends with frustration. AI transforms this daunting process into a simple, organized system where finding crucial details takes mere moments.

If you still rely on traditional methods, you're likely missing out on faster reviews, greater accuracy, and early risk detection. Understanding how AI fits into your document review process can lead to measurable efficiency gains and give your legal team the clarity it needs to move quickly and with precision.

What Is an AI Document Review?

AI-powered document review uses artificial intelligence to scan, sort, and analyze legal documents with speed and accuracy. It helps legal teams optimize legal contracts, extract key terms, identify risky clauses, and ensure compliance without getting lost in paperwork.

This process is powered by:

- Machine learning to detect patterns across contracts

- AI position creator to write an excellent job description

- Natural language processing to understand legal language

- Optical character recognition (OCR) to convert scanned text into searchable content

- Retrieval-augmented generation (RAG) to improve results using verified legal sources

Top Benefits of Using AI in Legal Document Reviews

The top benefits of using AI for document reviews are to:

Process documents faster without losing quality

Manual document review is time-consuming. Legal teams often spend hours tagging files, reviewing pages, and checking for red flags. AI makes this easier by automatically sorting contracts, identifying key terms, and organizing data in minutes. That means faster turnaround and better use of internal resources. Teams can move from sorting documents to making real decisions with less delay.

Spot errors and compliance risks early

AI uses natural language processing (NLP) and predictive coding to catch inconsistencies, missing clauses, and outdated terms. It highlights risky language, checks regulatory alignment, and flags documents that need attention.

When reviewing international contracts, AI compares document terms with current laws. Instead of going through long checklists, the system pinpoints where adjustments are needed. Teams stay ahead of compliance challenges with less effort. This helps reduce the risk of oversight without slowing down the process.

Lighten the load for legal teams

Repetitive tasks slow legal professionals down. Reviewing similar clauses, extracting data, or preparing standard documents can drain time that should be spent on strategic work.

With AI handling repetitive tasks, legal experts can focus on negotiations, advising clients, and managing risk. A paralegal using AI to update templates now spends more time reviewing deals and less time formatting files. It becomes easier for legal teams to focus on work that drives better outcomes.

| Document Review Task | Traditional | AI-Enhanced |

| Initial document sorting | Manual review (days) | Automated classification (hours) |

| Data extraction | Manual entry | Automated extraction with high accuracy |

| Compliance checking | Checklist review | Real-time automated verification |

| Risk assessment | Manual analysis | AI-powered pattern recognition |

Rather than replacing human expertise, AI complements it. Legal professionals can focus on nuanced issues while AI handles the bulk of document processing and preliminary analysis.

Save money while boosting output

Artificial intelligence helps reduce document review costs. Teams cut hours spent on manual work, leading to fewer billable hours wasted and less reliance on expensive support. Firms using AI tools have reported savings per case by automating early-stage reviews. This means better workload management and fewer delays during peak case periods.

According to a 2024 Thomson Reuters report, AI can help lawyers save up to 4 hours weekly, resulting in an estimated $100,000 in additional annual billable time per lawyer. These gains contribute directly to more substantial legal tech ROI, helping firms justify their investment in automation and scale their operations more efficiently.

AI Technologies Transforming Document Review

Legal work depends on details, but the volume of documents can overwhelm even the most organized team. AI helps reduce that pressure by turning complex legal text into structured, manageable insights.

Here are some AI-powered collaboration tools that are leading this shift: 2.

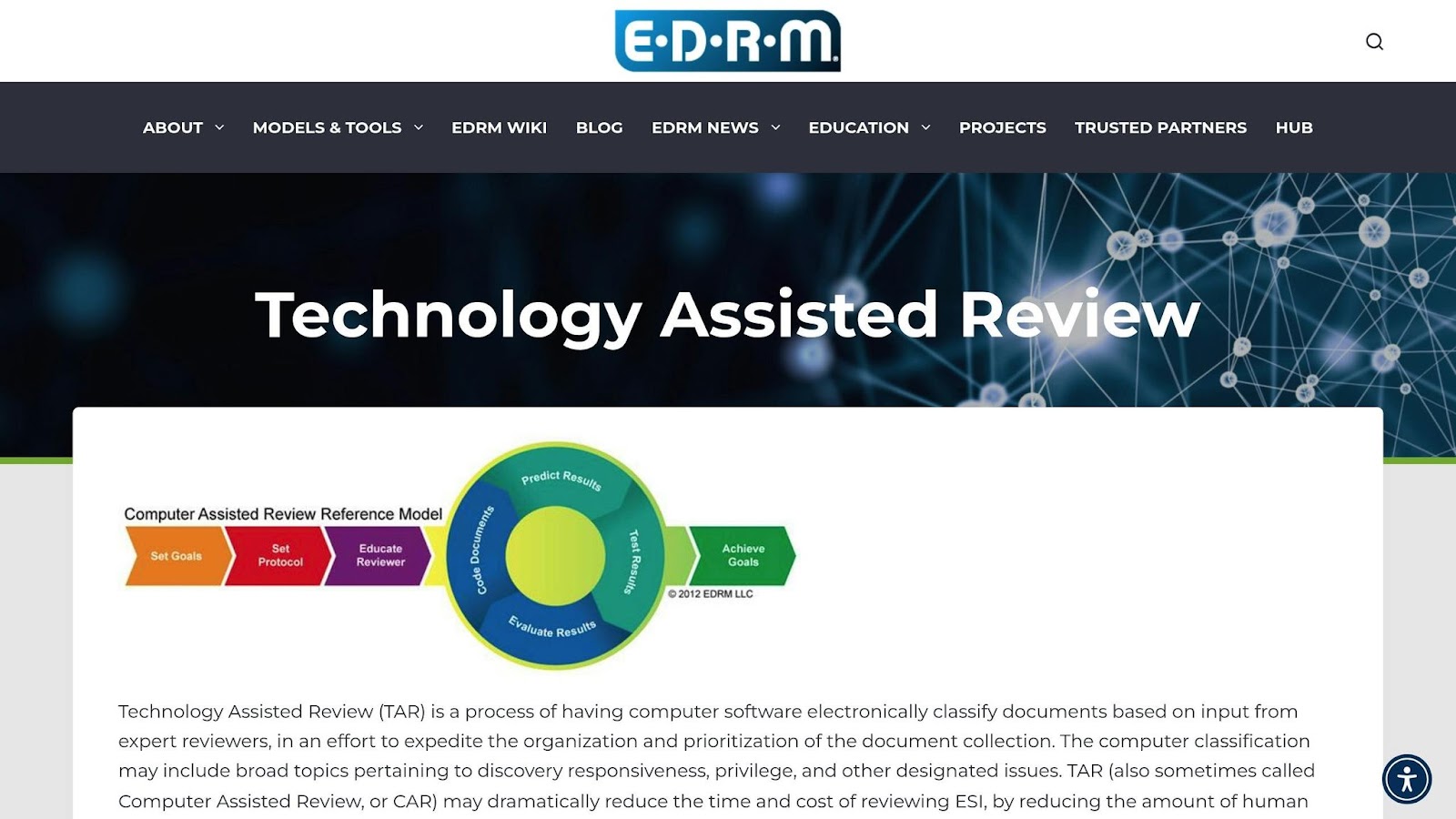

Technology-Assisted Review (TAR) Systems

TAR systems help legal teams focus on what matters when faced with thousands of documents. They use machine learning to help them organize and prioritize content without getting lost in the clutter.

TAR systems support legal work by:

- Predicting which documents are most relevant

- Learning from reviewer input to improve results

- Filtering out low-priority or irrelevant files

- Helping teams move faster without losing accuracy

Natural Language Processing (NLP)

Legal language can be challenging to interpret, even for experienced professionals. NLP helps AI read between the lines, interpret complex phrases, and flag anything out of place.

With NLP, legal teams can:

- Identifying non-standard terms in contracts

- Flagging missing or outdated clauses

- Extracting obligations and key dates automatically

Ensuring consistent language across multiple documents

AI-Powered Document Summarization

Legal documents are often lengthy, complex, and filled with dense language. When deadlines are tight, reviewing them manually can lead to delays, missed clauses, or overlooked risks. AI-powered summarization addresses this challenge by using natural language processing (NLP) and machine learning to generate concise, context-aware summaries without omitting critical content.

This technology extracts and condenses essential information such as key clauses, obligations, renewal terms, and risk indicators. It distinguishes between routine content and impactful language, allowing legal professionals to focus on the most critical sections.

| Use Case | Manual Review | AI Summarization |

| Contract review | Line-by-line reading | Summary with highlighted clauses |

| Internal briefings | Manual drafting of summaries | Automated, context-rich brief generation |

| Due diligence | Manual flagging of issues | AI identifies risks and terms automatically |

| Agreement comparison | Side-by-side document checks | Key differences surfaced in summary format |

By integrating summarization into legal workflows, teams reduce cognitive load, improve consistency, and accelerate analysis across high-volume matters. This enables faster decision-making and enhances review accuracy, especially in M&A, compliance audits, and multi-jurisdictional assessments.

How to Successfully Implement AI into Your Legal Workflows

Adding AI to your legal process should not require a complete system overhaul. Here’s a practical approach to making it work:

Step 1: Assessing Your Current Review Process

Before bringing in AI, examine how your team handles document reviews. Are they spending too much time sorting contracts or repeating similar reviews across departments?

Start by tracking where delays happen, where human errors are most common, and which tasks slow down daily operations. This helps identify where automation can have the most impact, whether sorting NDAs, spotting compliance issues, or reviewing standard agreements.

Step 2: Selecting the Right AI Tools

Once your pain points are clear, it’s time to choose software that solves those issues. Not every AI tool fits every firm, so focus on features that match your workflows.

The best AI tools for document review should offer:

- Smart search and filtering for quick document navigation

- Clause identification and extraction

- NLP capabilities for reviewing legal language

- Compliance checkers aligned with your jurisdiction

- Secure access and audit trails to maintain data integrity

If your team works across multiple systems, look for tools with solid integrations and scalable infrastructure.

Step 3: Staff Training and Adoption

No AI tool will succeed without a team that knows how to use it. Legal professionals don’t need to become developers but should feel confident using the platform and understanding its results.

A good rollout plan includes:

- Short, focused training sessions tied to everyday legal tasks

- Live walkthroughs with real documents

- Internal champions who support the team during the transition

- Ongoing support to answer questions and refine usage

When teams see how much time AI can save, they can adopt it into their routines quicker.

Step 4: Monitoring and Optimizing AI Performance

Once your system is in place, the work isn’t done. Legal teams must track how well AI tools perform and adjust as needed.

Some helpful metrics include:

- Review accuracy: How often does the tool flag the right issues?

- Turnaround time: How quickly are documents processed compared to before?

- Compliance alignment: Do the flagged documents meet legal standards?

- User adoption: Are legal staff consistently using the tool in their workflow?

Over time, these insights help you fine-tune settings, improve team usage, and boost legal tech ROI without the trial-and-error of manual review processes.

Common Challenges in Implementing Legal Document Review AI

Adopting AI can unlock real advantages, but like any major shift, it comes with a few hurdles. The good news is that these challenges are manageable with the right mindset and practical steps. The following are the two main challenges in implementing AI legal document review and how it can be integrated with legal teams.

Overcoming Resistance to AI

Legal professionals are trained to value precision and caution, so it’s natural for them to be skeptical of new technology, especially when it changes how core tasks are done.

The key to gaining support is showing how AI helps rather than replaces. Legal teams are likelier to adopt new tools when they see clear examples of AI saving time on repetitive work, reducing errors, and supporting faster reviews.

To encourage adoption:

- Start with low-risk pilot projects that allow teams to test the tool in real scenarios

- Provide hands-on demonstrations tailored to legal workflows

- Highlight small wins early, such as reduced time spent reviewing standard contracts

- Appoint team members who understand both the tech and legal processes to guide others

- Keep communication open and supportive as the team adjusts

Once professionals see the impact on their daily work, confidence grows, and adoption becomes easier.

Addressing AI Ethics and Bias

As helpful as AI is, it has regulatory implications that could pose a challenge. AI works based on the data it was trained on. The tool can produce flawed results if the training data includes flawed assumptions. For law firms, that’s a serious concern, especially when reviewing sensitive agreements or handling compliance matters.

Addressing this starts with transparency. Legal teams need to know how their AI tools make decisions, what data sources are used, and how risks are flagged. Regular reviews help ensure that the AI is working as intended and not making choices based on hidden bias.

Simple safeguards include:

- Auditing AI decisions regularly and documenting review patterns

- Choosing vendors that explain how their systems are trained and tested

- Including diverse training data to avoid one-sided assumptions

- Keeping humans in the loop for final decisions on flagged risks or clauses

AI works best when guided by clear ethical practices and human oversight. By implementing these checks early, firms can build trust in the technology and reduce risk while gaining all the benefits of automation.

Conclusion: AI’s Growing Role in Legal Document Review

AI is no longer a futuristic concept in legal work; it’s quickly becoming a foundational part of how documents are reviewed and managed. As legal matters become more complex and timelines continue to tig’s role is evolving from a helpful tool into a strategic pillar of modern legal operations.

Still, the value of AI depends on thoughtful integration. Tools that flag anomalies, detect patterns, or generate summaries provide leverage, but that leverage only turns into results when guided by the right expertise. Lawtrades enables this by connecting legal departments with professionals who understand the legal process and the technology driving AI-powered review. Their ability to structure workflows and interpret AI outputs ensures the system delivers a measurable impact.

Firms aligning this expertise with the right technology will be best positioned to lead, operating with speed, precision, and clarity across every document review stage.

Related posts

AI Ethics in Legal Risk Management

Using AI in legal risk management feels like relying on a fast but unpredictable assistant. It can sort through contracts, flag compliance risks, and predict legal exposure in seconds, but the consequences can be serious when that system makes a wrong call.

According to a study, 60% of organizations have attracted legal scrutiny because of decisions made by AI systems. That’s a significant concern for legal teams tasked with keeping operations compliant and defensible.

This is precisely why ethical oversight matters. In this article, we will discuss the key risks AI introduces in legal work and how your team can implement safeguards to avoid costly mistakes.

Key Ethical Challenges in Legal AI Systems

Even though many AI-powered collaboration tools are helping legal teams work faster and smarter, they bring their own set of ethical challenges. These issues directly impact fairness, trust, and legal teams' compliance with regulatory standards. Legal teams using AI tools must know and address these risks early.

The top ethical challenges legal teams face today include:

AI Bias and Unfair Outcomes

Bias often begins with the data. Many AI systems are trained using past legal cases, contracts, or historical decisions that already reflect bias. If the data is flawed, the AI will carry those same patterns into new reviews. The model’s design and where it’s used also matter. AI trained in one region or industry may perform poorly in another.

For example, an AI reviewing employment contracts may flag a clause as unfair simply because it isn’t common in its training data, not because it's legally wrong. That leads to unnecessary edits or delays. Left unchecked, AI bias can turn a helpful tool into a liability.

Lack of Transparency in AI Decisions

Legal teams are used to explaining why a clause is risky or why a document needs revision. With AI, that clarity isn’t always there. Some systems deliver decisions without showing how they were made, making it challenging for lawyers to trust or defend the results in front of clients and regulators.

Integrating workflow automation with legal tech requires a high level of transparency because AI becomes another risk without transparency. Teams need tools that show how decisions were made, what data was used, and why specific results were flagged. Explainability builds trust and helps legal teams stay in control.

Risks to Legal Data Security

AI systems often require access to a firm’s most sensitive documents. If that data isn’t handled carefully, it can lead to breaches, leaks, or regulatory violations. Protecting legal data means securing systems from hackers, limiting internal access, encrypting files, and following strict legal storage requirements.

The entire firm is at risk if an AI system stores or processes sensitive documents without proper safeguards. Data security failures can break client trust and trigger significant fines. Once data is exposed, there's no taking it back.

How to Build Ethical Legal AI Systems

Legal teams can't afford to treat AI like a black box. To avoid reputational harm or regulatory penalties, your system must be built on ethical principles from the start. That means using quality data, testing for fairness, and constantly reviewing performance.

Strengthen Your Data Preparation

Poor data leads to flawed outcomes. About 85% of AI failures can be traced to low-quality or insufficient data. Fixing the data pipeline is one of the most effective ways to build responsible AI for legal risk management.

A well-structured data preparation process lays the foundation for ethical automation. Here’s what it should look like:

| ###### Step | ###### Purpose | ###### Action Point |

| Bias Audits | Identify imbalances or harmful patterns | Review datasets for skewed legal case representation |

| Balanced Sampling | Ensure fair distribution | Include diverse jurisdictions, client types, and case types |

| Data Enrichment | Fill gaps with validated sources | Add verified regulatory records or public legal rulings |

| Quality Control | Maintain data integrity | Schedule regular checks for errors and inconsistencies |

This structure helps legal teams create a strong foundation before training any AI model.

Improve Fairness During AI Training

Once the data is clean, the focus shifts to how your model is trained. Testing for fairness at this stage reduces the risk of biased outcomes.

Use cross-validation methods to evaluate model performance across various legal scenarios. Include diverse case samples during training to confirm that the model behaves consistently across all input types.

Microsoft’s Fairlearn is one of the most widely used toolkits for assessing and improving fairness. It allows legal tech teams to test different model outcomes and adjust where bias is detected. Integrating tools like this into your AI workflow improves long-term reliability and compliance.

Verify Outputs and Maintain Oversight

AI systems are not "set and forget." Ongoing review is essential to ensure the system remains compliant, accurate, and fair. This step focuses on keeping outputs in check long after deployment.

Below is a simple framework for verifying AI outputs and keeping a consistent feedback loop:

| ###### Review Area | ###### Frequency | ###### Goal |

| Bias Detection Tools | Weekly | Track drift or changes in fairness |

| Manual Review | Monthly | Evaluate outputs against legal standards |

| User Feedback Loops | Ongoing | Catch overlooked issues and improve trust |

| Outcome Analysis | Quarterly | Analyze long-term system performance |

Ethical oversight keeps your AI system aligned with legal responsibilities while protecting against silent failures.

Legal Governance and Compliance Standards

Ethical AI doesn’t end at design; it’s a continuous responsibility. For legal teams using AI in risk management, aligning with governance frameworks and legal requirements is non-negotiable. Here are some key standards and systems legal departments need to stay compliant and audit-ready.

Governance Frameworks to Follow

Several organizations have introduced governance frameworks to guide ethical AI deployment. Two of the most widely referenced include:

- NIST AI Risk Management Framework (AI RMF): This U.S.-based framework helps organizations identify and manage risks in AI systems. It covers everything from transparency and accountability to safety and fairness.

- ISO/IEC 23894: A global standard offering guidance for managing risks specific to AI-based systems. It complements existing data and privacy frameworks, making it ideal for legal teams with international operations.

Adopting these frameworks helps establish internal accountability. Most high-functioning legal departments set up oversight committees composed of legal, compliance, and technical professionals. These teams are responsible for tracking AI decisions, resolving ethical concerns, and reviewing incident reports, ensuring nothing slips through unnoticed.

Meeting Legal and Regulatory Requirements

AI governance only works when it's aligned with real legal obligations. That means staying ahead of evolving data protection laws, keeping documentation ready for inspection, and adapting to new ethical expectations.

Here’s what your compliance strategy should include:

- Data Privacy Standards: Encrypt sensitive legal data, enforce role-based access, and comply with jurisdiction-specific laws like GDPR and CCPA.

- Documentation and Audit Readiness: Maintain a complete record of AI training data sources, model updates, risk assessments, and system logs. This documentation must be available for internal and external reviews.

- Ethical Obligations Across Jurisdictions: In cross-border cases, AI must respect differing legal ethics. Some regions require AI explainability or restrict data use. Having legal professionals review AI decisions helps you stay compliant in every jurisdiction you operate in.

A clear governance structure protects your clients and your firm from preventable risks.

Conclusion: Ethical AI Begins with the Right Support

Ethics is the groundwork that determines whether the system should be trusted at all. Without it, even the most advanced AI tools become liabilities, introducing bias, weakening compliance, and eroding client trust. That’s why legal teams focus less on speed alone and more on building systems that meet regulatory expectations and reflect professional integrity.

Support from platforms like Lawtrades makes this easier. By connecting teams with legal professionals who specialize in AI governance and compliance, Lawtrades helps organizations shape ethical frameworks that scale with their operations. With the proper guidance, legal departments can implement AI confidently, knowing they’re backed by the structure and oversight needed to stay aligned with evolving standards.

Related posts

Legal KPIs vs Metrics: Key Differences

You track the number of contracts reviewed this week, you know the average turnaround time, and there’s a spreadsheet for almost everything. However, when leadership asks whether Legal is meeting its strategic goals, the numbers fall short.

This is where many legal teams get stuck: confusing activity with progress. Metrics reflect motion. KPIs reflect impact.

The distinction is not cosmetic. It defines whether Legal is seen as a reactive support function or a forward-driving business unit. Metrics help manage workflows; KPIs prove whether those workflows are moving the business in the right direction.

If your legal team is buried in dashboards but unclear on impact, this guide will help you reframe what performance looks like. You’ll learn how to distinguish KPIs from metrics, align both with legal and business objectives, and start measuring outcomes that matter, not just activity.

What KPIs and Metrics Mean

Legal departments use performance data to assess effectiveness, manage risk, and guide operational strategy. This data is typically split into two categories: key performance indicators (KPIs) and metrics. Each plays a distinct role in evaluating and improving legal function.

What Are KPIs?

Key performance indicators are high-level measurements tied directly to strategic objectives. They evaluate whether legal operations meet business-aligned goals and often serve as benchmarks for executive reporting.

Common examples include:

- Cost per legal matter: Tracks the average expenditure associated with resolving a legal matter. This is especially useful in measuring efficiency across different case types.

- Percentage of contracts completed within Service Level Agreements (SLAs): Measures how consistently the legal team meets service-level expectations. A drop in this KPI may signal resourcing or process issues.

- Regulatory compliance rate: This rate indicates how well the organization adheres to legal and regulatory requirements. Falling below target thresholds may highlight systemic compliance risks.

Each KPI connects legal activities to business impact, offering insight into overall departmental effectiveness.

What Are Metrics?

Metrics capture operational data points that explain how work is being done. They focus on specific tasks, throughput, or service performance. While not all metrics are tied directly to business goals, they provide context for understanding and improving KPIs.

Examples include:

- Number of contracts reviewed per week: Reveals team workload and output levels, which may inform resource planning.

- Average time to process legal requests: Tracks operational efficiency and helps identify workflow bottlenecks.

- Total legal spend by practice area: Provides visibility into cost distribution, which is useful for budgeting and vendor management.

- Volume of pending litigation matters: Helps assess case backlog and litigation exposure.

Metrics act as the diagnostic tools behind KPI performance, guiding daily decision-making and operational refinement.

Understanding the distinction between KPIs and metrics is foundational for legal departments aiming to improve performance, demonstrate value, and align closely with enterprise objectives.

Key Differences Between KPIs and Metrics

Understanding how KPIs and metrics differ is essential for structuring effective legal performance frameworks. While both serve measurement purposes, they operate at different decision-making levels and have distinct implications for strategy and execution.

| Aspect | KPIs | Metrics |

|---|---|---|

| Purpose | Assess alignment with strategic legal and business goals | Track and quantify specific activities within legal operations |

| Scope | Department-wide or cross-functional outcomes | Task-level performance or workflow benchmarks |

| Time Frame | Typically long-term (quarterly or annually) | Often short-term (daily, weekly, or monthly) |

| Impact on Goals | Directly tied to strategic objectives | May support KPIs indirectly or provide operational insight |

| Example | Reduce outside counsel spending by 15% over 12 months | Track average hourly rate by law firm per month |

KPIs serve as strategic benchmarks while metrics provide operational data. For example, if a legal team sets a KPI of 95% SLA compliance for contract turnaround, supporting metrics might include average review time and the number of contracts that missed the SLA.

Metrics inform, validate, and contextualize KPIs but are not goals in themselves. Legal teams may monitor dozens of operational metrics across departments, but the KPIs help them focus on the outcomes that drive business value.

A legal department may track dozens of metrics across various workflows, but only a handful, typically 5 to 7 KPIs, are tied directly to strategic objectives. Prioritizing these key indicators helps maintain clarity and ensures the team stays focused on outcomes that matter most to the business.

The Interrelationship Between KPIs and Metrics

Because KPIs and metrics serve different purposes, it's easy to focus on one and overlook the other. But in a high-functioning legal department, both are essential. KPIs show where you're going. Metrics show how you're getting there.

To drive measurable progress, you need a system that connects operational activity with strategic outcomes. Metrics give you the granularity to monitor daily processes. KPIs consolidate that information to reflect how those efforts support long-term business goals.

Example:

If your legal team aims to reduce contract turnaround time by 20%, you can’t rely on the KPI alone. Supporting metrics like average time from contract submission to initial review, number of revision cycles, and delay frequency provide the detail needed to identify bottlenecks and adjust workflows in real time.

By aligning the two, you ensure that every tracked activity is tied to a strategic result and that reliable, actionable data supports every result. This alignment transforms reporting into real performance management.

Setting Up Effective Measurements

Your legal metrics must do more than report numbers to get real value from your performance tracking system. They must reflect your business priorities, drive improvement, and guide decisions. Here’s how to build a measurement framework that does exactly that.

Align Metrics with Legal and Business Goals

Begin by mapping your team’s metrics to your company's broader goals. Metrics should reflect the areas where legal can deliver the most value: risk mitigation, cost control, operational agility, and client responsiveness.

Examples:

- If your priority is risk management, track metrics like unresolved compliance issues or time to respond to regulatory requests.

- For cost control, monitor average matter spending, external counsel fees by matter type, and total budget variance month-to-month.

- To improve operational efficiency, measure contract lifecycle times, frequency of bottlenecks, and legal request fulfillment rates.

- For internal client satisfaction, track turnaround time for business requests, number of escalations, and volume of service-level breaches.

Let’s say your legal department is pressured to cut outside counsel spending by 20% this year. Supporting metrics might include cost per matter, average timekeeper rates, and volume of high-rate billers used per quarter. These tell you what’s driving spending and where to intervene.

Translate Priorities into SMART Goals

Once you've identified the right metrics, convert them into SMART goals—Specific, Measurable, Achievable, Relevant, and Time-bound. This ensures that each goal is actionable and tied to results.

| SMART Element | Legal Application Example |

|---|---|

| Specific | "Reduce contract review time for NDAs." |

| Measurable | "By 30% based on current 12-day average." |

| Achievable | "Using automated intake and clause libraries." |

| Relevant | "Supports our larger goal of speeding deal cycles." |

| Time-bound | "Achieve by Q3 of the current fiscal year." |

Example:

If your team wants to speed up the contracting process, your SMART goal might be: “Reduce average contract turnaround time for procurement contracts by 30%, using automated approval workflows, by Q4 2025.”

Use Both Historical and Predictive Metrics

To fully understand performance and make better decisions, combine:

Lagging Indicators (look back):

- Final cost of closed matters

- Time to close litigation cases

- SLA compliance rates last quarter

Leading Indicators (look ahead):

- Number of high-risk contract clauses flagged during review

- Upcoming workload forecasts by business unit

- Planned resource allocation by matter complexity

For example, if your goal is to improve SLA compliance, lagging indicators will tell you how often SLAs were missed last quarter. Leading indicators, such as the current backlog or upcoming request volume, help you prepare and stay ahead.

When you track both, you gain insights into past performance and influence what happens next.

Conclusion

Tracking contracts and monitoring turnaround time may show how busy your legal team is, but busyness isn’t the same as progress. Actual progress is when operational activity moves the business forward, which requires aligning granular metrics with strategic KPIs.

KPIs reflect outcomes that matter. Metrics inform the journey. When structured correctly, they work together to drive visible, defensible performance and align with business priorities.

To make this shift, you need clearly defined numbers supported by legal talent and systems capable of turning them into tangible outcomes. It’s the combination of insight and execution that moves performance forward.

Lawtrades connects legal departments with experienced operations professionals who can help design the right KPIs, structure performance dashboards, and translate metrics into strategic recommendations. Whether you're building a legal ops function from scratch or optimizing a mature one, the right expertise turns reporting into a competitive advantage.

By embedding performance measurement into your legal workflows, you gain more than insight; you gain control, clarity, and strategic influence. That’s how modern legal teams lead with precision.

Related posts

ROI of On-Demand Legal Talent Platforms

What if your legal team could scale expertise without adding headcount and cut spending without sacrificing quality?

Traditional staffing models often lock teams into rigid costs, slow hiring cycles, and one-size-fits-all solutions. Meanwhile, legal demands shift weekly, and the pressure to do more with leaner resources never lets up.

That’s why more legal departments are turning to on-demand talent platforms.

These platforms offer a responsive, cost-efficient way to access vetted legal professionals across specialties. Whether you need short-term contract review support, regulatory expertise, or ongoing operational help, the model flexes with your needs and gives full transparency into hours, costs, and output.

For teams managing fluctuating workloads or trying to make smarter resource decisions, on-demand legal staffing offers a compelling return: fewer overhead commitments, faster execution, and measurable control over legal spend.

But how do you quantify the return on this model compared to traditional staffing, and is your team ready to make that shift?

Understanding On-Demand Legal Talent Platforms

On-demand legal talent platforms are digital services that allow companies to quickly access freelance legal professionals without relying on traditional law firms or full-time hires. These platforms are built to serve evolving legal needs such as:

- Contract review and negotiation

- Regulatory research and filings

- Mergers and acquisitions due diligence

- Litigation and discovery support

- Internal investigations and compliance work

Lawtrades is one of the most prominent platforms in this space. It connects legal departments with highly experienced attorneys and legal professionals for flexible, on-demand work. The platform focuses on speed, specialization, and integration with in-house legal operations.

Key features of Lawtrades include:

- Vetted legal talent: Professionals are screened based on expertise, responsiveness, and industry alignment

- Flexible engagement models: Choose hourly, project-based, or long-term support without fixed commitments

- Workflow integration: Manage legal tasks, monitor hours, and track deliverables directly through the platform

- Cost transparency: Clear pricing with no overhead fees or hidden markups

Companies use Lawtrades to scale their legal teams during periods of high demand or when specialized skills are needed. Instead of hiring full-time or engaging large firms, they gain access to legal professionals who understand their business and can deliver efficiently.

This model reduces legal costs, speeds up project delivery, and allows in-house teams to stay focused on strategic priorities.

The Growing Market for Alternative Legal Services

The rise of on-demand legal talent platforms is part of a broader transformation in how legal services are delivered. According to the 2025 Thomson Reuters ALSP Report, the global market for alternative legal services providers (ALSPs) has reached $28.5 billion, driven by demand for more agile, specialized, and cost-efficient support.

This change reflects a shift away from relying solely on traditional law firms. Legal departments are redistributing work toward flexible service models that blend better with evolving business operations and resource strategies.

Several factors are fueling this momentum:

-

Operational cost controls

ALSPs provide access to high-quality legal support without the ongoing expense of full-time hires or fixed firm retainers. This allows legal teams to align spending with workload demands. -

Need for speed and adaptability

Projects related to M&A, regulatory deadlines, or rapid product expansion often require faster turnaround times than conventional hiring models can deliver. ALSPs offer near-immediate access to professionals who are ready to begin with minimal onboarding. -

Specialized legal expertise

Many legal teams need subject matter experts in areas like fintech compliance, international IP, or emerging data privacy laws. ALSPs allow teams to engage senior-level talent for focused engagements. -

Unbundling of legal work

Legal departments are increasingly segmenting their workflows. Routine or high-volume tasks are delegated externally, while core strategic counsel is retained internally. ALSPs fit well within this approach by delivering precise results within defined scopes.

As legal teams integrate contract management systems, eDiscovery platforms, and AI-powered workflows, ALSPs such as Lawtrades become even more aligned with modern operations. The professionals available on these platforms are often experienced in using legal tech tools, which helps teams stay efficient and digitally agile.

Key Benefits Contributing to ROI

On-demand legal talent platforms generate measurable returns by improving how legal departments manage resources, deliver outcomes, and adapt to changing priorities. Beyond basic cost avoidance, these platforms unlock structural advantages that translate into operational and strategic value.

Precision Resourcing

One core benefit is the ability to allocate legal resources with a high degree of accuracy. Rather than defaulting to generalist support or overstaffing, legal leaders can engage professionals tailored to each task. This reduces both overwork and underutilization. By aligning skillsets directly with project needs, teams achieve more focused execution and cleaner handoffs between in-house and external contributors.

Cycle Time Reduction

Legal throughput is a critical but often overlooked component of business velocity. Legal review or documentation delays can stall product launches, regulatory filings, or transactions. On-demand platforms significantly reduce cycle time by eliminating the bottlenecks tied to conventional staffing models. Projects begin faster, progress is tracked in real time, and deadlines become more predictable.

Load Balancing Without Operational Disruption

When internal bandwidth is maxed out, legal departments often face a trade-off: delay work or compromise quality. On-demand legal professionals provide a buffer without introducing disruption. Temporary gaps due to employee leave, high-volume events like end-of-quarter contract reviews, or short-term regulatory deadlines can all be handled without changing team structure or long-term budgets.

Strategic Optionality

The platform model also creates room for experimentation and strategic moves. Legal departments can test new support models, trial specialists in emerging areas like ESG compliance or cryptocurrency regulation, or run pilot programs before committing to more significant investments. This controlled flexibility makes it easier to innovate within legal operations while maintaining accountability.

Enhanced Forecasting and Spend Control

Legal spend becomes more predictable since work is scoped and billed based on actual deliverables or hours. Dashboards and tracking tools on platforms like Lawtrades help monitor project status, time allocations, and budget in real time. This level of visibility supports better forecasting, improved vendor management, and easier justification of legal spend to finance teams.

These benefits go beyond transactional savings. They reposition legal teams as proactive, efficient units that can adjust rapidly to evolving business needs without compromising quality or oversight.

Direct Comparison Results

Apparent structural differences exist between on-demand legal talent models and traditional staffing approaches. These differences influence legal spending, resource efficiency, and how teams manage variable workloads.

Cost Structure Comparison

| Aspect | On-Demand Legal Talent | Traditional Staffing or Law Firms |

|---|---|---|

| Hourly Rates | $130–$350 per hour depending on specialization | $400–$800 per hour for law firm professionals |

| Overhead Costs | No costs for benefits, workspace, or onboarding | Includes full employee benefits, office space, and training programs |

| Minimum Commitments | Flexible agreements tied to specific deliverables | Annual contracts or fixed retainer requirements |

| Scaling Costs | Adjusts based on project scope and demand | Increases significantly with each additional hire or retainer |

This structure allows legal departments to align spending with workload. Payment is tied to actual services rendered, without recurring obligations. Teams avoid carrying unnecessary overhead when projects end or shift.

This approach creates more control over resource planning and provides financial predictability across periods of high and low legal activity. Work can begin when needed, conclude when complete, and scale in either direction without renegotiation or restructuring.

Challenges and Considerations

While on-demand legal talent platforms provide clear operational and financial advantages, successful integration depends on careful planning and internal readiness. These engagements often require adjustments to workflows, team dynamics, and oversight protocols. Failure to account for these factors can limit the effectiveness of the model.

Alignment with Legal and Compliance Standards

External professionals must work within your organization’s established legal and regulatory frameworks. This includes understanding jurisdictional requirements, internal approval structures, and risk tolerance thresholds. To maintain consistency, clearly define engagement scopes, approval checkpoints, and document handling procedures before work begins. A lack of alignment can lead to rework, compliance gaps, or sign-off process delays.

Confidentiality and Data Security

Legal professionals often access sensitive contracts, intellectual property, and privileged communications. Without proper controls, this access poses security and confidentiality risks. Legal departments should establish access protocols, use secure document-sharing systems, and require platform-level confidentiality agreements or NDAs. Work environments must be auditable, and data should be encrypted in transit and at rest.

Collaboration with Internal Teams

Onboarding external contributors into fast-moving legal teams can disrupt established communication flows. Delays in information sharing or unclear task ownership can reduce efficiency. To avoid this, designate internal points of contact, standardize task assignment tools, and establish shared expectations for reporting, meeting cadence, and work format.

Platform Selection and Fit

Choosing a platform requires more than evaluating pricing or talent availability. Look for the following:

- Verified vetting and credentialing of professionals

- Integrated project tracking and time logging tools

- Secure infrastructure and GDPR/CCPA compliance

- Options for client feedback and post-engagement reviews

These features help legal departments maintain control and visibility throughout the engagement lifecycle.

Task Suitability and Scope Management

Not every legal task is suitable for outsourcing. High-stakes matters involving strategic decision-making, regulatory interactions, or executive communications may require internal oversight. On-demand talent works best for defined scopes with clear deliverables and limited institutional complexity.

Before assigning work, assess the task's scope, dependencies, and risk exposure. If the task requires deep familiarity with internal history or cross-functional coordination, in-house execution may be more appropriate.

By addressing these considerations early, legal teams can fully capture the benefits of flexible legal support while minimizing friction and exposure.

How to Measure ROI of On-Demand Legal Talent

Measuring return on investment (ROI) from on-demand legal talent requires a structured approach beyond cost comparison. It involves quantifying financial savings, operational efficiency, and strategic output in relation to the resources invested. Legal departments should treat this evaluation as part of their broader legal operations performance framework.

Key ROI Metrics

To calculate ROI, consider both direct and indirect value contributions using the following indicators:

-

Cost Efficiency Ratio

Compare total expenditure on on-demand professionals to equivalent costs using law firms or internal hires. This includes hourly billing, project duration, and the volume of completed deliverables.

Formula:

Cost Efficiency = (Traditional Cost – On-Demand Cost) / Traditional Cost × 100 -

Time to Completion

Track average time taken to complete specific legal tasks (e.g., contract review, due diligence) when using on-demand talent compared to internal processing or firm turnaround times. Shorter timelines contribute to faster business decisions and reduced cycle lag. -

Utilization Accuracy

Measure the percentage of billed hours aligned with active, outcome-driven work. Unlike salaried roles, on-demand engagements should show minimal idle time.

Formula:

Utilization Accuracy = (Hours Worked on Deliverables / Total Hours Billed) × 100 -

Project Outcome Quality

Use standardized feedback forms to rate the quality of delivered work across multiple dimensions—completeness, legal accuracy, format, and internal team satisfaction. These metrics can be used to score providers and forecast performance. -

Operational Impact Score

Assign weighted values to strategic outcomes such as risk mitigation, contract turnaround, or successful regulatory filings. This score gives a broader view of how legal work contributes to business goals.

For instance, a mid-sized SaaS company preparing for acquisition engaged two on-demand M&A specialists for contract due diligence. The project spanned three weeks.

- On-Demand Legal Spend: $18,000

- Law Firm Quote for Same Scope: $56,000

- Time Saved: 15 days faster than firm timeline

- Contracts Reviewed: 120

- Internal Review Score: 9.2/10 average rating

ROI Calculation:

($56,000 - $18,000) / $18,000 × 100 = 211% ROI

In addition to cost savings, the company completed the due diligence window ahead of schedule, giving executives extra time to negotiate deal terms. The ability to redeploy internal legal staff to other pre-acquisition tasks added further strategic value.

This type of outcome should be logged into a centralized legal operations dashboard, allowing teams to track performance trends and refine future resourcing decisions. Measuring ROI consistently turns flexible legal support from a tactical choice into a data-backed operational strategy.

Conclusion: Maximizing ROI from On-Demand Legal Talent Platforms

Have you decided to make your first hire of an on-demand legal professional? Legal departments must approach flexible staffing with a structured, performance-driven model to realize a meaningful return on investment. ROI is not determined by cost savings alone. It is calculated through a combination of measurable variables, including efficiency gains, resource utilization, turnaround consistency, and alignment with business objectives.

Legal functions integrating on-demand talent into their operations with defined scopes, centralized reporting, and ongoing performance evaluation are better positioned to achieve sustained value. Key practices include applying outcome-based metrics, using utilization benchmarks to allocate resources, and standardizing workflows for repeatable engagements.

Many legal teams trust Lawtrades to support this model. For example, 1Money extended the capacity of a single in-house counsel by incorporating external legal talent through Lawtrades, enabling timely support across corporate, commercial, and product matters. Udemy similarly optimized internal capacity by relying on Lawtrades to manage contract review workloads at scale, allowing internal counsel to focus on strategic risk management.

Optimizing the ROI of on-demand legal talent platforms requires more than access to external professionals. It depends on how well each engagement supports measurable legal outcomes, integrates with internal processes, and evolves with operational demands. When used with strategic intent, these platforms become a repeatable asset for driving efficiency, controlling costs, and scaling legal capacity with precision.

Related posts

EU-US Data Privacy Framework: Compliance Guide

Cross-border data transfers are essential to modern business operations, but they carry significant legal and regulatory risks, especially when transferring personal data from the EU to the US. The EU-US Data Privacy Framework (DPF), effective July 10, 2023, was introduced to restore legal certainty for transatlantic data flows following the invalidation of the Privacy Shield.

This framework establishes a structured pathway for US-based organizations to demonstrate adequate protection of EU personal data under the GDPR. It imposes stricter oversight, purpose limitation, and enforceable rights for EU data subjects while also addressing key concerns raised by the Court of Justice of the European Union regarding US surveillance practices.

This guide provides a technical and practical overview of the DPF, including eligibility requirements, certification procedures, compliance controls, and how the DPF interacts with other transfer mechanisms like Standard Contractual Clauses (SCCs). Whether you're preparing for certification or maintaining an existing compliance posture, this resource outlines what it takes to align your business with the latest transatlantic data protection standards.

How to Join the DPF

Organizations seeking to transfer personal data from the EU to the US under the EU-US Data Privacy Framework must complete a formal self-certification process administered by the U.S. Department of Commerce. This process confirms that your organization adheres to the DPF Principles and has the necessary privacy governance in place to protect EU data subjects.

Below is a detailed breakdown of the certification steps:

1. Initial Assessment

Begin with a comprehensive internal audit of your organization’s data lifecycle:

- Map all data flows involving EU personal data, including collection points, processing systems, storage locations, and any transfers to third parties.

- Identify compliance gaps in your current data protection policies and procedures relative to DPF requirements.

- Evaluate vendor relationships, especially third-party processors and subprocessors, to ensure their alignment with DPF obligations.

This assessment forms the baseline for remediation and documentation efforts ahead of certification.

2. Update Your Privacy Policy

Your public-facing privacy policy must reflect your organization’s commitment to the DPF Principles. Ensure it includes:

- The purposes for which personal data is collected and processed

- A description of data subject rights, including access, correction, deletion, and dispute resolution options

- Information on data retention policies and how long personal data is kept

- A clear outline of data transfer mechanisms, including onward transfers to third parties

- Contact information for privacy inquiries or complaints

- A statement indicating your participation in the DPF, including a reference to the Department of Commerce’s certification list

The policy must be easy to understand, legally accurate, and accessible to both EU individuals and regulatory authorities.

3. Register with the Department of Commerce

To certify, submit your application through the official Data Privacy Framework program website:

- Include your organization’s legal name, contact details, and business sector.

- Upload or link to your updated privacy policy.

- Complete the required self-certification statements, attesting that your organization complies with the DPF Principles.

- Pay the applicable annual fee based on your organization’s size.

Once approved, your organization will be listed on the Department of Commerce’s DPF certification directory. You must recertify annually and keep your policies and internal practices up to date.

Post-Certification Obligations

Certification is not the final step; it initiates an ongoing compliance obligation. To maintain eligibility:

- Ensure internal policies and training programs reflect DPF standards

- Keep detailed records of data practices, third-party disclosures, and user request logs

- Monitor and respond to regulatory guidance or legal developments affecting DPF requirements

Proper documentation, clear accountability structures, and regular reviews will support long-term compliance and reduce legal exposure.

Required Business Compliance Measures

To maintain a valid certification under the EU-US Data Privacy Framework (DPF), organizations must implement specific operational controls and documentation standards that demonstrate adherence to its principles. These business compliance measures are not optional; they form the basis of accountability under the framework and are subject to regulatory scrutiny.

Privacy Policy Updates

Your privacy policy serves as a public declaration of your organization’s data-handling practices. Under the DPF, it must clearly communicate how personal data is collected, used, retained, transferred, and safeguarded.

Key elements to include:

- Purpose specification: Explain why personal data is collected and how it will be used

- Data subject rights: Detail the rights available to EU individuals (access, correction, deletion, portability) and how they can be exercised

- Retention policy: State how long personal data is retained and the criteria used to determine the duration

- Third-party sharing practices: Disclose whether data is shared with service providers or affiliates, including the nature of such transfers

- Point of contact: Provide up-to-date contact details for privacy-related inquiries or complaints

- DPF participation statement: Indicate your certification status and reference the Department of Commerce’s DPF list

The privacy policy must be written in clear, legally precise language and updated annually or whenever a material change in processing occurs.

Data Protection Requirements

A strong security infrastructure is a fundamental requirement for DPF compliance. Organizations must demonstrate technical and organizational controls that protect personal data from unauthorized access, misuse, or loss.

Encryption Standards

- Use AES-256 or stronger for encrypting data at rest

- Implement TLS 1.3 for data transmitted over public networks

- Follow defined key management protocols to avoid exposure of encryption keys

Access Management

- Implement Role-Based Access Control (RBAC) to enforce least privilege access.

- Conduct quarterly access reviews to ensure only authorized personnel retain access.

- Enforce Multi-Factor Authentication (MFA) for systems containing sensitive or regulated data.

Breach Response Protocol

- Notify supervisory authorities within 72 hours of discovering a breach involving EU personal data.

- Maintain a documented incident response plan, including escalation procedures and mitigation steps.

- Perform regular breach simulation tests to evaluate readiness and response accuracy.

Staff training, monitoring systems, and formal documentation must support these technical controls to ensure defensibility during audits.

User Data Rights Management

Organizations must enable EU data subjects to exercise their rights efficiently with a clear, verifiable workflow in place. The DPF requires responses to all rights-based requests within 30 calendar days.

| Right Type | Response Time | Required Actions |

|---|---|---|

| Access | 30 days | Provide a machine-readable copy of all personal data held |

| Correction | 30 days | Amend inaccurate data and notify all affected processors |

| Deletion | 30 days | Permanently delete personal data across all systems and confirm completion |

| Portability | 30 days | Deliver data in a structured, commonly used format |

Ensure you have:

- A request intake system with identity verification

- A tracking mechanism to document request dates, assigned owners, actions taken, and closure dates

- Audit logs that demonstrate ongoing compliance with response timelines and procedures

Third-Party Coordination

When personal data is transferred to processors or service providers, your organization remains accountable under the DPF. To maintain compliance:

- Establish contractual obligations requiring third parties to assist with rights-based requests

- Maintain a record of all processors and subprocessors handling EU personal data

- Document all communications and outcomes related to third-party cooperation in handling access, correction, deletion, or portability requests

Well-documented third-party procedures and agreements are essential for demonstrating full lifecycle data stewardship. They also reduce exposure during external audits or enforcement actions.

By implementing these business compliance measures, organizations can establish a defensible, repeatable framework for maintaining DPF certification and supporting long-term data protection objectives.

DPF and Other Transfer Methods

While the EU-US Data Privacy Framework (DPF) provides a legal basis for transferring personal data from the EU to certified U.S. organizations, it is not a universal solution. Many organizations operate across multiple jurisdictions, engage with non-certified third parties, or manage data types that fall outside the scope of DPF. In these scenarios, integrating other transfer mechanisms—primarily Standard Contractual Clauses (SCCs)—becomes necessary to maintain GDPR compliance.

Using SCCs with DPF

Organizations may need to use SCCs alongside the DPF in the following situations:

1. Partial DPF Coverage

- When transferring data to U.S. entities that are not DPF-certified

- When transferring EU personal data to non-EU countries not covered by an adequacy decision

- When processing special categories of data or sensitive datasets that require additional safeguards

2. Multi-Jurisdictional Operations

- For businesses with global infrastructure that involves cross-border data flows beyond the EU-US corridor

- When using vendors or subprocessors located in countries without adequacy decisions or DPF participation

- In multi-party data processing arrangements, where a combination of compliance tools is needed to manage risk

The combined use of DPF and SCCs ensures data protection obligations are met across all data transfer scenarios and legal environments.

Combining Compliance Methods

Your data transfer strategy must be scalable and adaptable when operating under multiple legal frameworks. This requires aligning DPF and SCC implementation across technical, contractual, and organizational controls.

Data Flow Mapping

Create and maintain detailed flow diagrams that document:

- Which transfers are covered by the DPF (e.g., EU to U.S. certified entities)

- Which require SCCs (e.g., EU to non-certified U.S. processors or third countries)

- Where overlaps occur, requiring layered protections such as Transfer Impact Assessments (TIAs) or additional contractual clauses.

| Transfer Type | Primary Mechanism | Secondary Safeguard |

|---|---|---|

| EU → U.S. (certified entity) | DPF | Not required |

| EU → U.S. (non-certified) | SCCs | TIA recommended |

| EU → Other Countries | SCCs | Country-specific requirements |

| Multi-party Data Flows | DPF + SCCs | Data Processing Agreements (DPAs) |

Documentation Requirements

Maintaining defensible documentation is a core principle of DPF and GDPR accountability. Organizations should:

- Track DPF certification status, recertification dates, and historical changes

- Maintain a central register of active SCCs, including parties, scope, and transfer types

- Conduct and archive Transfer Impact Assessments (TIAs) where applicable

- Document internal and external audits that assess data transfer compliance controls

These records support regulatory inquiries, demonstrate proactive risk management, and strengthen internal governance.

Unified Compliance Strategy

A fragmented compliance approach increases exposure to legal and operational risk. Instead, legal and privacy teams should develop a unified strategy that integrates both DPF and SCC requirements across the data lifecycle:

- Align privacy notices with the specific obligations of each transfer mechanism

- Standardize user rights response procedures, regardless of transfer mechanism

- Create centralized breach notification protocols that satisfy both EU and U.S. obligations

- Train internal stakeholders and external processors on the applicable frameworks and required safeguards

This alignment reduces redundancy, ensures legal consistency, and improves audit readiness across jurisdictions. A unified compliance strategy built on DPF and SCCs positions organizations to manage global data transfers with confidence and regulatory integrity.

Anticipating Regulatory Shifts and Managing Operational Risk